RSS Feed

RSS Feed

|

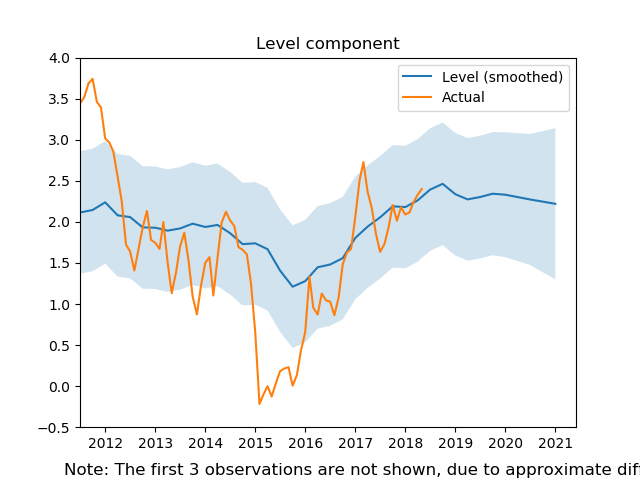

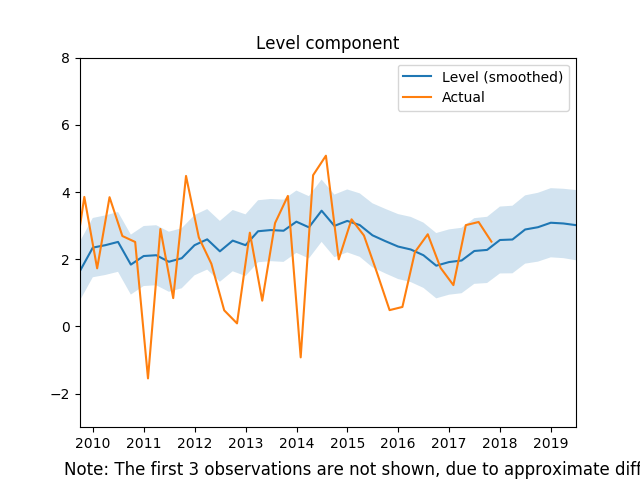

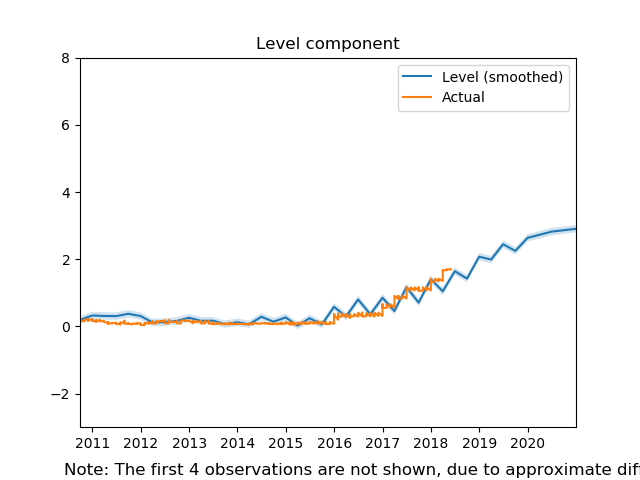

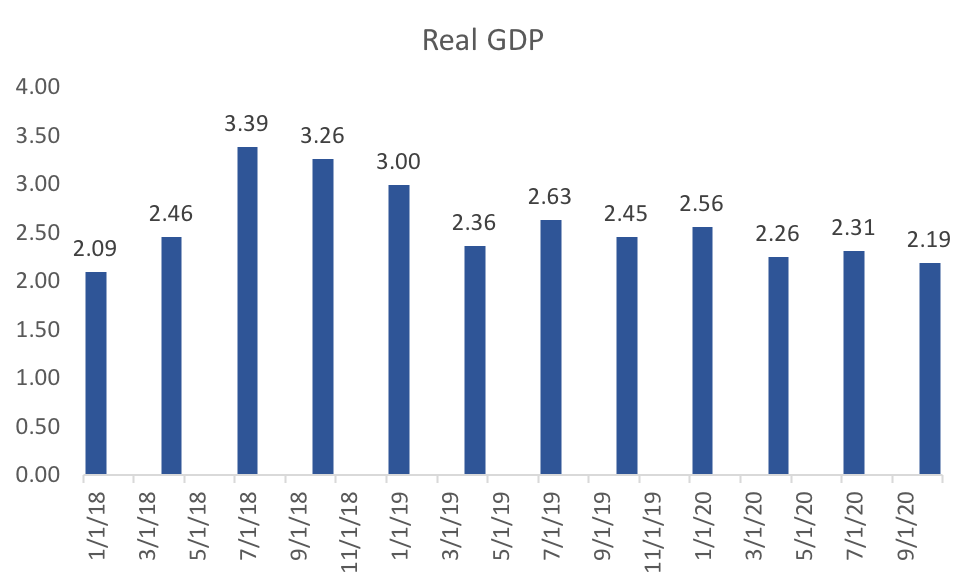

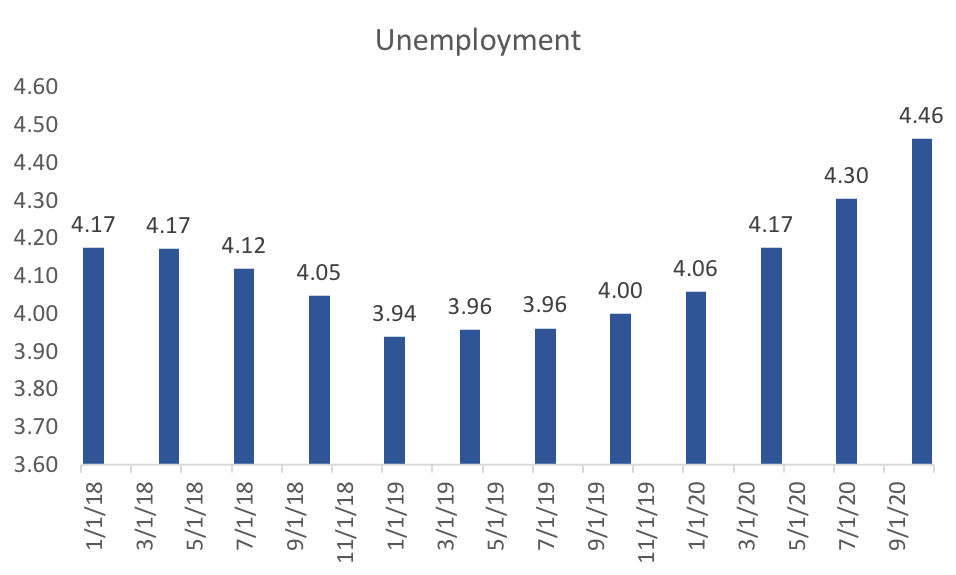

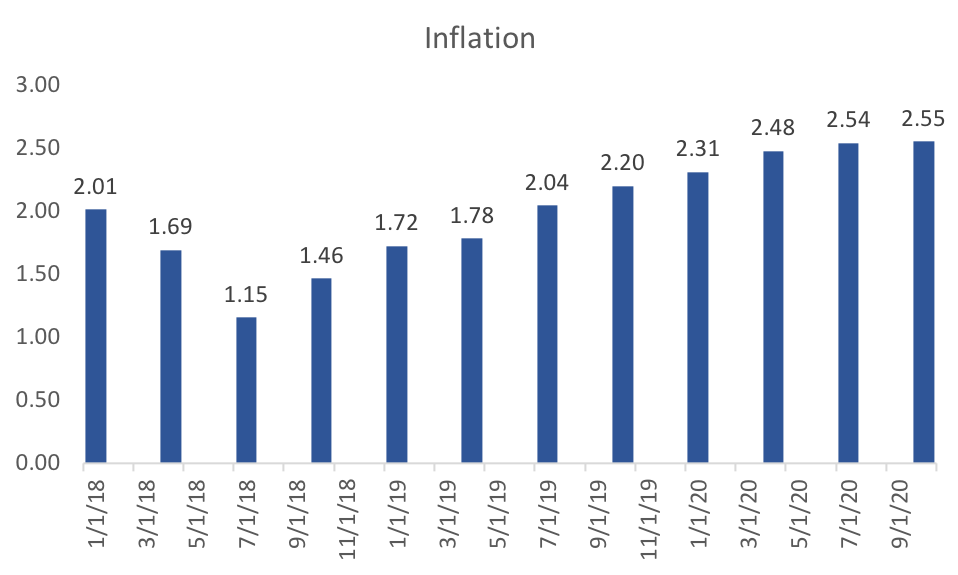

Using the most recent data including updated aggregate expectations, I have a new set of headline forecasts. First quarter data on international trade and finance have yet to be released, so these forecasts still rely on estimates of the Q1. Second quarter real GDP has dropped significantly (almost half a percent) from last month, whereas first-quarter forecasts increased to fall in line with the advance estimate. The end of 2018 still looks to be quite strong, before mellowing to long-run average growth in 2020.  Despite an apparent level shift (the newest unemployment data suggests my Q1 forecast is too high by 0.2 percentage points), my unemployment forecasts see further declines into 2019 before steadily climbing in 2020. That acceleration in unemployment is consistent with a significant recession beginning in the third or fourth quarter of 2020.  My model's forecasts of inflation suggest that the Fed's projected rate increases will keep inflation in check through 2019. There is a lot less variability in this set of projections compared to last month. The decline in inflation through 2018 seems robust, as does its eventual rise in 2020.  To round off this months forecast, I include the aggregate estimates of Inflation, GDP, and the federal funds rate. Inflation and GDP expectations remain high despite a (well-founded) belief of a rising federal funds rate.

0 Comments

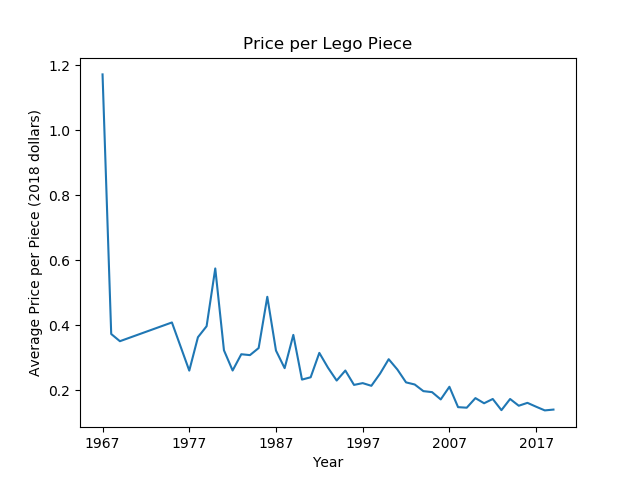

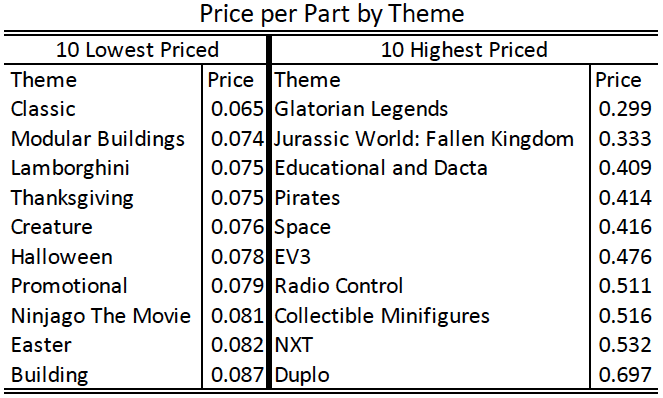

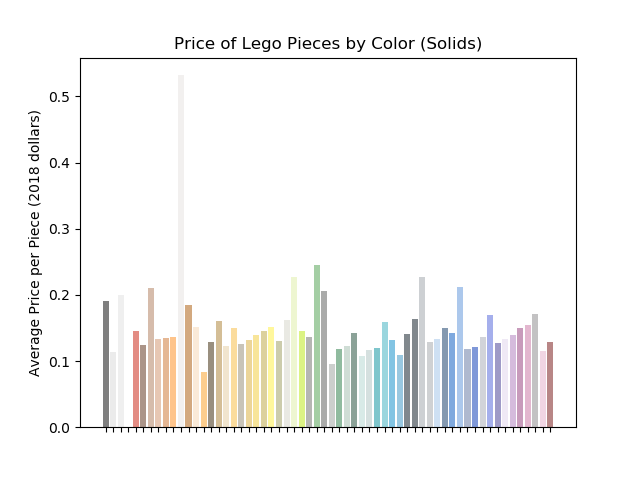

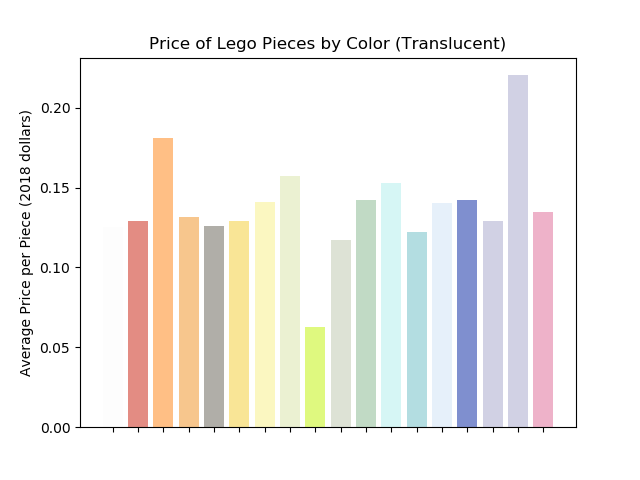

I love playing with Legos. I love playing with data. So when I got a chance to play with Lego data, I had a ton of fun. I have seen analysis of Lego prices (this 2013 article on lego is my favorite), but I thought I might be able to do something different, with the most recent data. Using the rebrickable database, for detailed set information, and a scrape of the brickset website, for retail prices, I created a dataset of real price per piece, that is I control for inflation. Like many people who have looked at Lego prices, the real price per piece does appear to be declining over time:  To dig further into the data I restricted my analysis to the last 10 years. Sorting the data by theme we see that the cheapest sets are the special holiday sets and themes with very large sets. I was surprised that the Modular Buildings were so cheap. Classic, makes sense because they are the most basic bricks, but the Modular Building theme typically has many specialty pieces.  Most of the highest priced themes are also not to surprising, the sets that have electrical circuitry are more expensive. I was surprised by Pirates and Space being so high up on the list though. However, I wanted to have a little fun. The rebrickable dataset gives the inventory for each set, and their colors. Using the frequency of the color in each set I reweigh the price per piece by the frequency of color. The graph below shows the price by color for all the non-translucent pieces.  If we look at translucent colors, it does look as though, in general, those colors are slightly more expensive:  I can also break down price by individual piece and again the prices more or less follow expectations. Very small pieces are cheap, large pieces with electronics are more expensive.

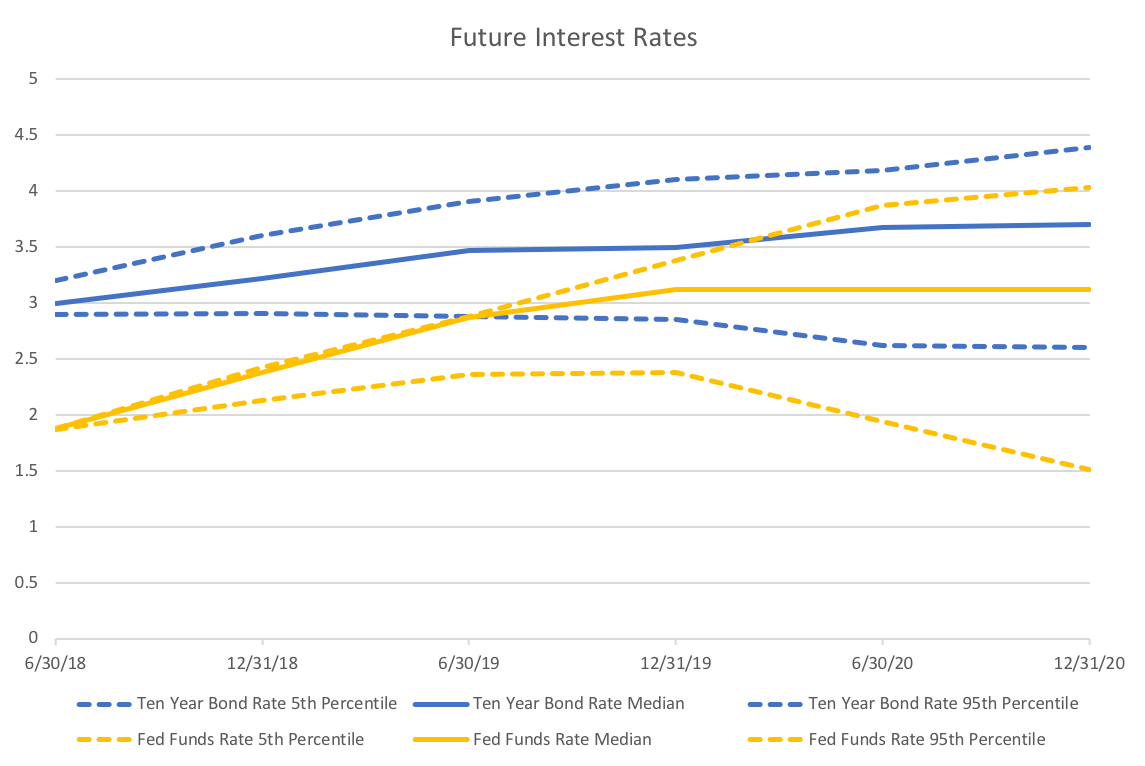

So if your goal is to expand your lego collection, get those modular and classic sets, and enjoy your Lego builds! Another relatively quiet month in terms of economic news. The recent data has not done much to shift the views of forecasters very significantly. One of the special questions in this months survey was regarding the timing of the next recession. Ben Leubsdorf of the WSJ does a great job discussing those responses. The big movers this month are crude oil price expectations, which jumped 5.5 dollars for June 2018, and the yield curve spread, which narrowed some more. Oil prices through the end of 2020 are expected to rise but with diminishing amounts, with December 2020 forecasts only rising 1.9 dollars. The yield curve spread is actually quite fascinating as I have noted in past reports.  The graph above shows the yield curve tightening through 2020. More importantly, the variability of these forecasts is interesting as well. The difference between the 5th and 95th percentiles grows dramatically for the fed funds rate but is much more stable for the ten-year bond rates. It is unclear whether it is policy uncertainty or economic uncertainty that is driving this difference. However, it is strange that forecasters predict that the long rate will not respond, at least not one for one, to the stated Fed goal of raising rates at least two more time by the end of the year.

Another curiosity: even though the majority of forecasters expect a recession in 2020, they don't seem to think that the Fed will respond to it. If they did I would expect the median fed forecast to at least be fall from June 2020 to December 2020. However, the recession timing predictions are more or less consistent with the consensus unemployment forecasts hitting their low in mid to late 2019. |

Archives

May 2018

Categories

All

|