RSS Feed

RSS Feed

|

A quick post on the second installment of aggregate forecasts we look at real GDP Growth. As with the inflation forecasts in an earlier post, this measure aggregates several sources of real GDP expectations. Unfortunately there fewer sources and for now I hesitate to include the various Fed nowcasts. The graph below shows the historical real GDP growth rates and the aggregated expectations:  And here is the raw data:  Finally let's zoom in on the last few years and the latest projections:  These aggregated forecasts suggest a robust 2018 and 2019. I suspect, however, that as those longer run forecasts will start to drift further down as the Fed raises rates in response to a tighter labor market.

0 Comments

The February WSJ forecasts are in and, in general, we are seeing good news. First off, 2018 Q1 expected GDP growth is up a quarter percent to 2.6 and the expected unemployment rates through 2020 all fell. The trough of unemployment is still hovering around mid 2019. Expected payrolls forecast rose by almost 8400, strengthened by the robust January employment report.

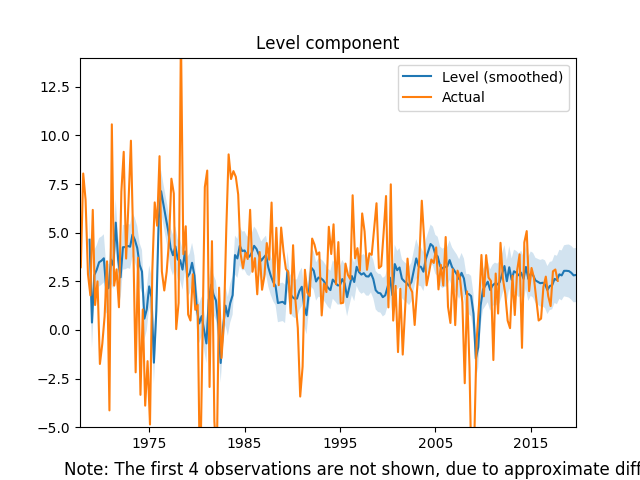

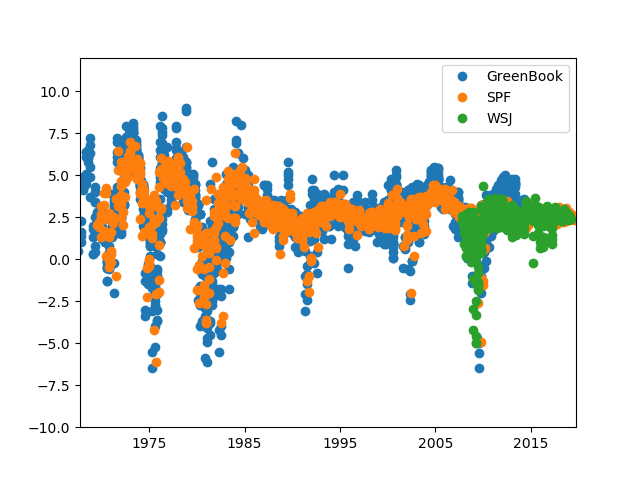

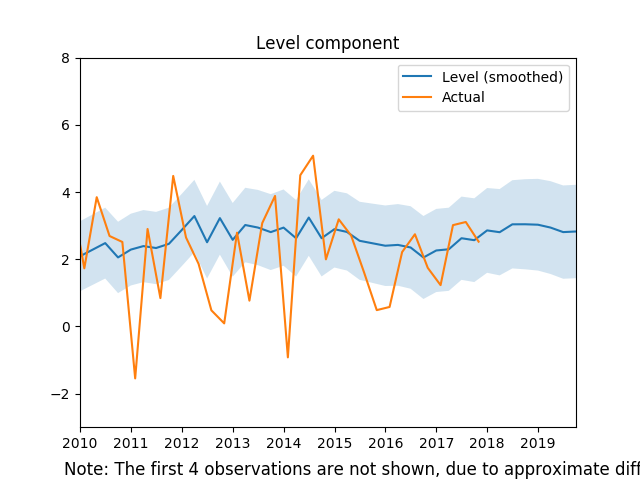

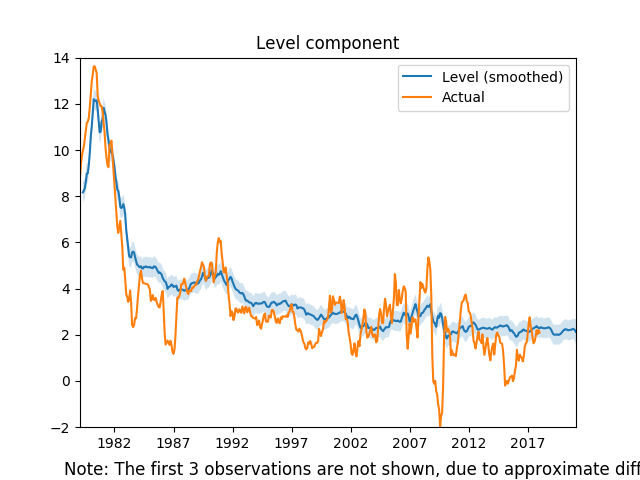

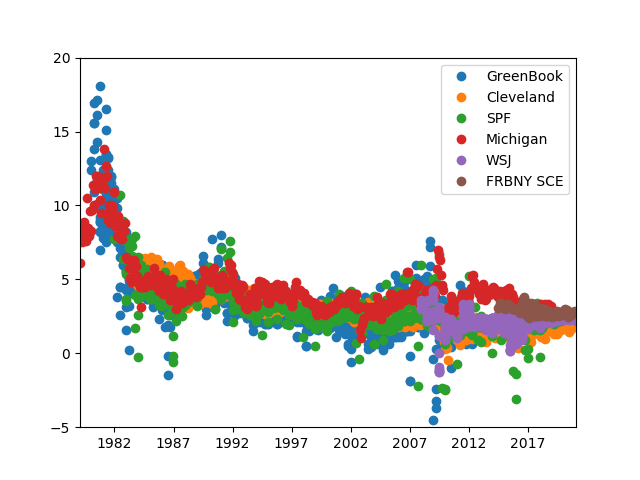

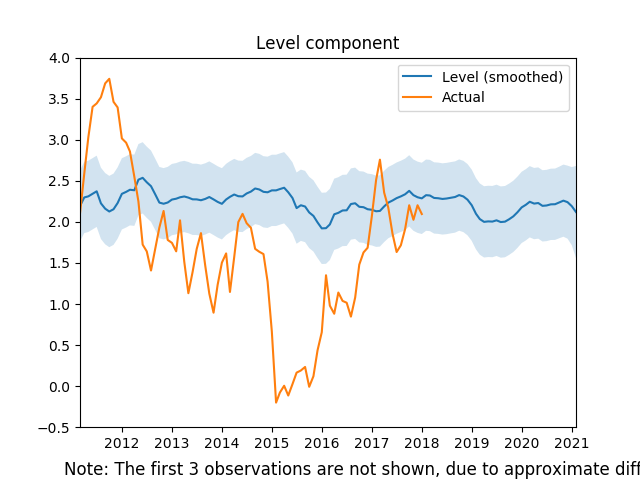

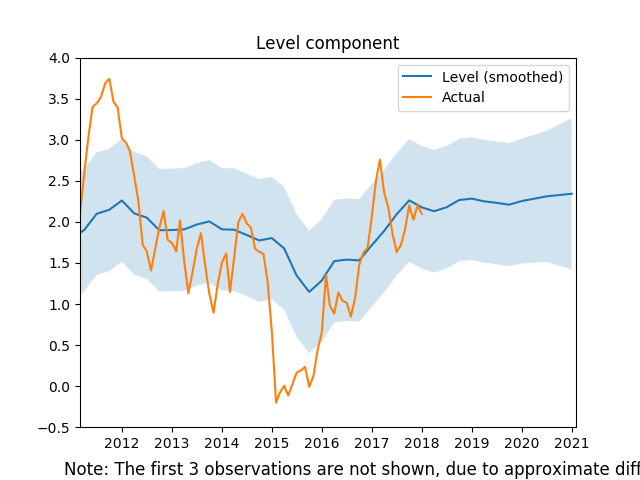

Inflation expectations increased again, standing firmly above 2 percent. Expected housing starts are more or less unchanged, but housing price forecasts for 2018 and 2019 both rose a tenth of a percent. We also saw a huge increase in crude oil expectations as almost all future prices rose by more than 2 dollars, with price expectations above 60 dollars for the next two years. Finally, consensus recession expectations rose, but still remain low, with less than a 14 percent chance of a recession in the coming 12 months. As I have noted in previous reports, December and January Reports, the spread between the expected future federal funds rate and the ten-year bond rate has been tightening. This month, ten-year bond rate forecast all rose by over a tenth of a percent, whereas consensus expected Federal funds rate increases were more modest. This is good news for monetary policy makers, because they will be able to use the long end of the yield curve when the next recession begins. However, in the short term, particularly given the recent sell off of stocks, this presents a potential head wind against our waning economic recovery. I have started a new project with the goal of generating several series that aggregate expectations of macroeconomic variables. This post describes the inflation expectations series. Below I have plotted the results relative to actual year-over-year CPI inflation.  This series combines six different inflation expectations series: Federal Reserve Greenbook forecasts, Survey of Professional Forecasters, NY Fed Survey of Consumer Expectations, WSJ Survey, Cleveland Fed Inflation Expectations, and the Michigan Survey of Consumers. There are typically multiple forecasts for any given month over many horizons. To construct the series I create an average weighted by the inverse of the forecast horizon. Then in order to strip away some of the seasonal shocks I pass the resulting data through and unobserved components model. Here is the raw expectations data:  We can see that only the last few years of the series incorporate the NY Fed and the WSJ forecasts, and the Greenbook survey has a 6 year lag. As such the most interesting part of this new measure is the last several years of data:  While the low inflation in 2015 did impact expectations (with a lag) the broad trend shows that inflation expectations are quite stable and slightly above 2 percent. This is good news for the Fed, but this series is influenced by Fed forecasts, so I dropped both the Greenbook and the Cleveland Fed forecasts in the graph below:  Interestingly, there is an even larger impact due to the 2015 drop in inflation, and it appears as if consumers and professional forecasters actually have lower inflation expectations in general.

While these graphs are useful, the methodology used in constructing the aggregated inflation expectations necessarily lost a lot of information. In the future, I would like to not only have the series for each month, but also the forecasts over the preceding 3 year horizon. With that information we could not only see what was happening to expectations, but also how those expectations of a particular point in time were evolving. Please let me know your thoughts... |

Archives

May 2018

Categories

All

|