RSS Feed

RSS Feed

|

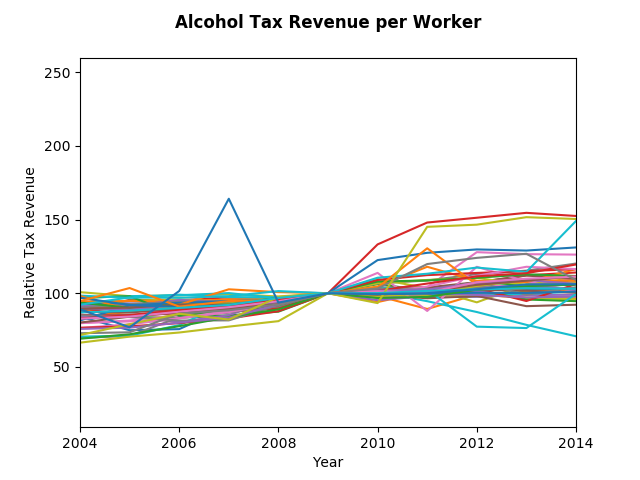

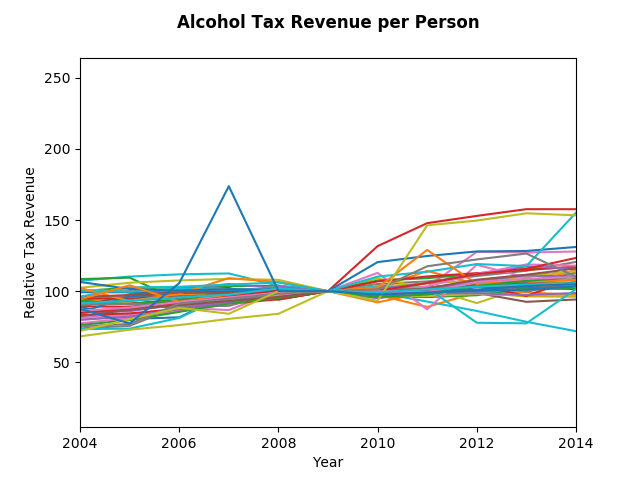

Endogeneity, or the chicken and the egg problem. Previously addressed in a post on Housing Prices in the US, this time we exam alcohol. Do we drink more during and after and recession because we are depressed? Or does the fall in income curtail our ability to purchase alcohol? Coming into this analysis, it seemed likely that the former was true, turns out, the latter seems to be true during the great recession. The state level data collected comes from the Tax Policy Center and GeoFred. Surprisingly alcohol tax revenue per person has been increasing by about 2 percent per year, more or less keeping up with inflation. The graphs below show relative changes in Alcohol Tax Revenue per Person and per Worker in all 50 states (and DC), with a base year of 2009. While there are certainly a few states that saw large increase post recession, it is unclear whether we are observing increasing or decreasing growth rates. To address that question we can calculate average growth for each state in the five years prior to 2009 and and the five years after. Calculating the difference of the average we find that growth of alcohol tax revenue per person declined by 0.35 percentage points while per worker it declined by 1.59 percentage points. If instead we choose 2007 as the mid point, so that the 18 months of the recession are part of the post period, the numbers for per person and per worker are a 1.46 percentage point decline and a 0.11 percentage point increase, respectively. Those results suggest that it's likely that the income effect dominates the "feeling depressed" effect.

Naturally with a rough analysis like this there are some caveats. Tax revenue is not the same as consumption, but I suspect they are highly correlated, particularly when the tax laws have not changed. To really be sure of this result one would need to control for increases (and decreases) in alcohol sales tax rates. In addition, the recession hit states disproportionately. A more proper analysis would take that into account. Finally, this analysis also lacks a way to control for substitution effects, that is, a switch from expensive to cheap alcohol.

0 Comments

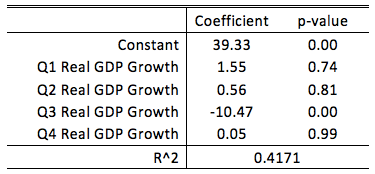

WSJ Economic Forecast participants report the probability of a recession within the next 12 months. The consensus of the June survey participants has that probability at 16 percent. It appears that Q3 GDP growth appears to play a critical role in forecasters recession probabilities. The table below reports the results of a simple regression.  A forecaster who predict zero GDP growth in Q3 would place, on average, a 40 percent probability on the chance of a recession in the next 12 months. For every one percent increase in predicted Q3 GDP growth, that average recession probability would decrease by 10 percentage points. The other quarters do not appear to have a statistical relationship with recession probabilities.

Taken altogether, while a recession does not appear likely to these forecasters, the third quarter plays a pivotal role in these forecasts. The current consensus is 2.6% growth in the third quarter, only slightly below Q2 expectations. If we see weakness leading into the third quarter, we can expect forecasters to start increasing the probability of a recession. |

Archives

May 2018

Categories

All

|