RSS Feed

RSS Feed

|

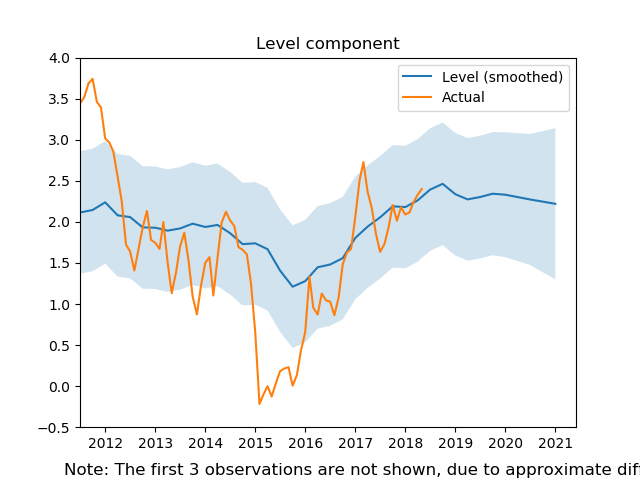

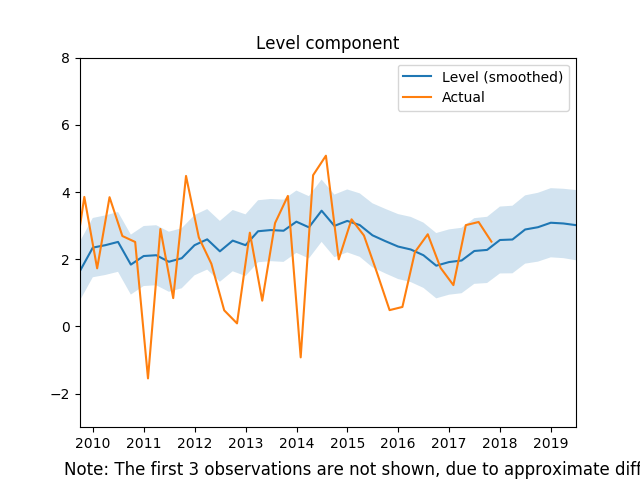

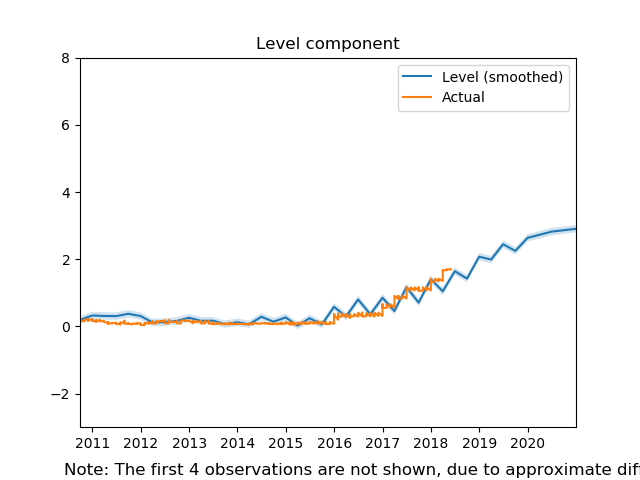

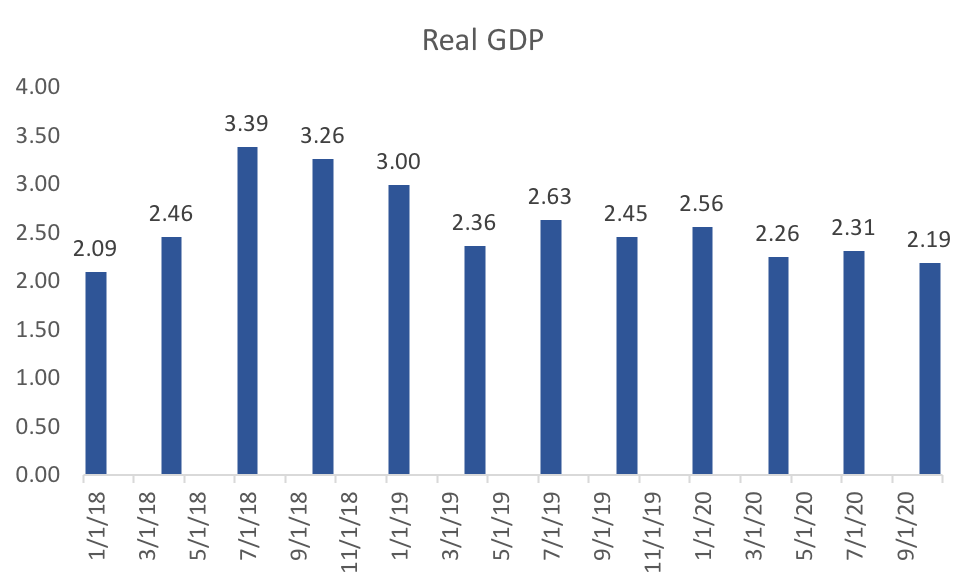

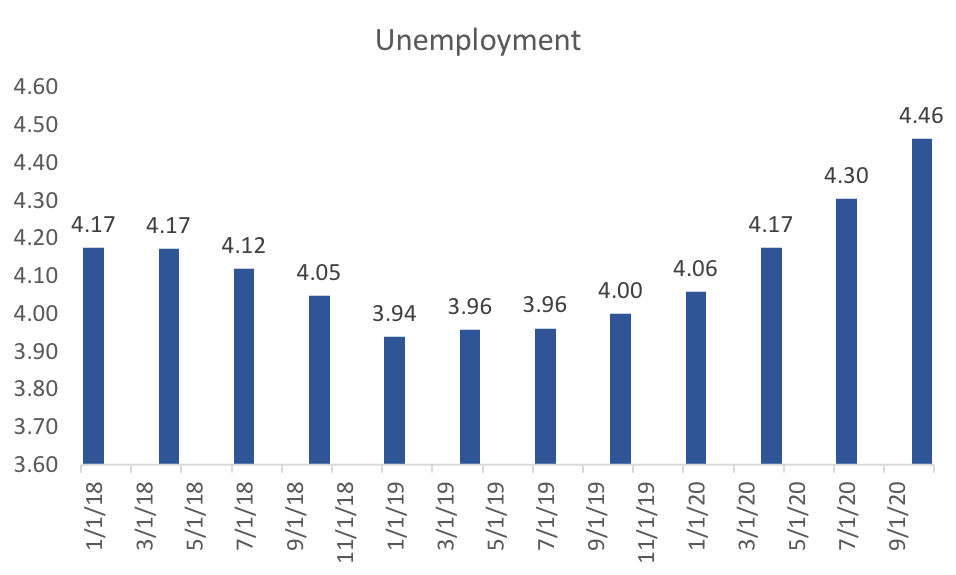

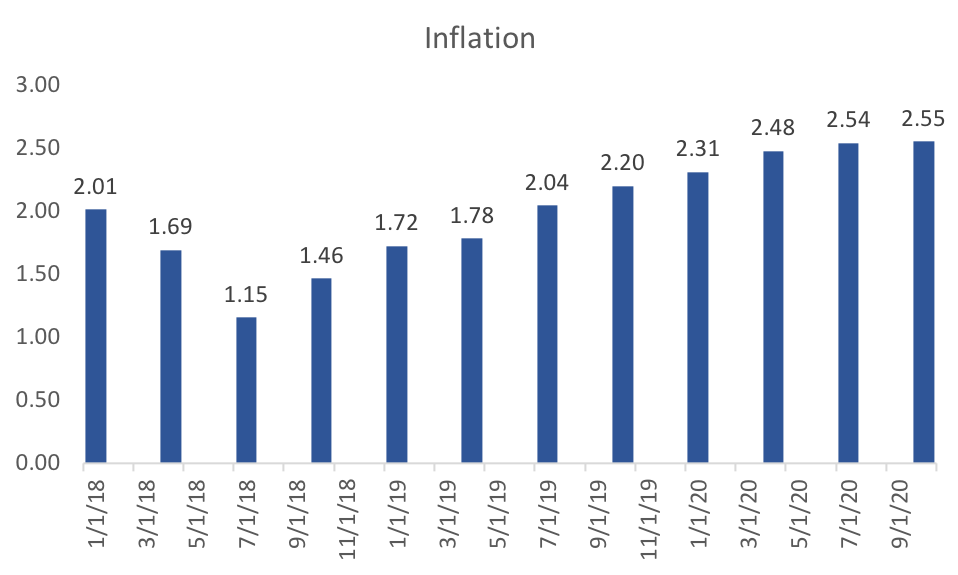

Using the most recent data including updated aggregate expectations, I have a new set of headline forecasts. First quarter data on international trade and finance have yet to be released, so these forecasts still rely on estimates of the Q1. Second quarter real GDP has dropped significantly (almost half a percent) from last month, whereas first-quarter forecasts increased to fall in line with the advance estimate. The end of 2018 still looks to be quite strong, before mellowing to long-run average growth in 2020.  Despite an apparent level shift (the newest unemployment data suggests my Q1 forecast is too high by 0.2 percentage points), my unemployment forecasts see further declines into 2019 before steadily climbing in 2020. That acceleration in unemployment is consistent with a significant recession beginning in the third or fourth quarter of 2020.  My model's forecasts of inflation suggest that the Fed's projected rate increases will keep inflation in check through 2019. There is a lot less variability in this set of projections compared to last month. The decline in inflation through 2018 seems robust, as does its eventual rise in 2020.  To round off this months forecast, I include the aggregate estimates of Inflation, GDP, and the federal funds rate. Inflation and GDP expectations remain high despite a (well-founded) belief of a rising federal funds rate.

0 Comments

Leave a Reply. |

Archives

May 2018

Categories

All

|